Toronto Market Report

2024 Fourth Quarter Update

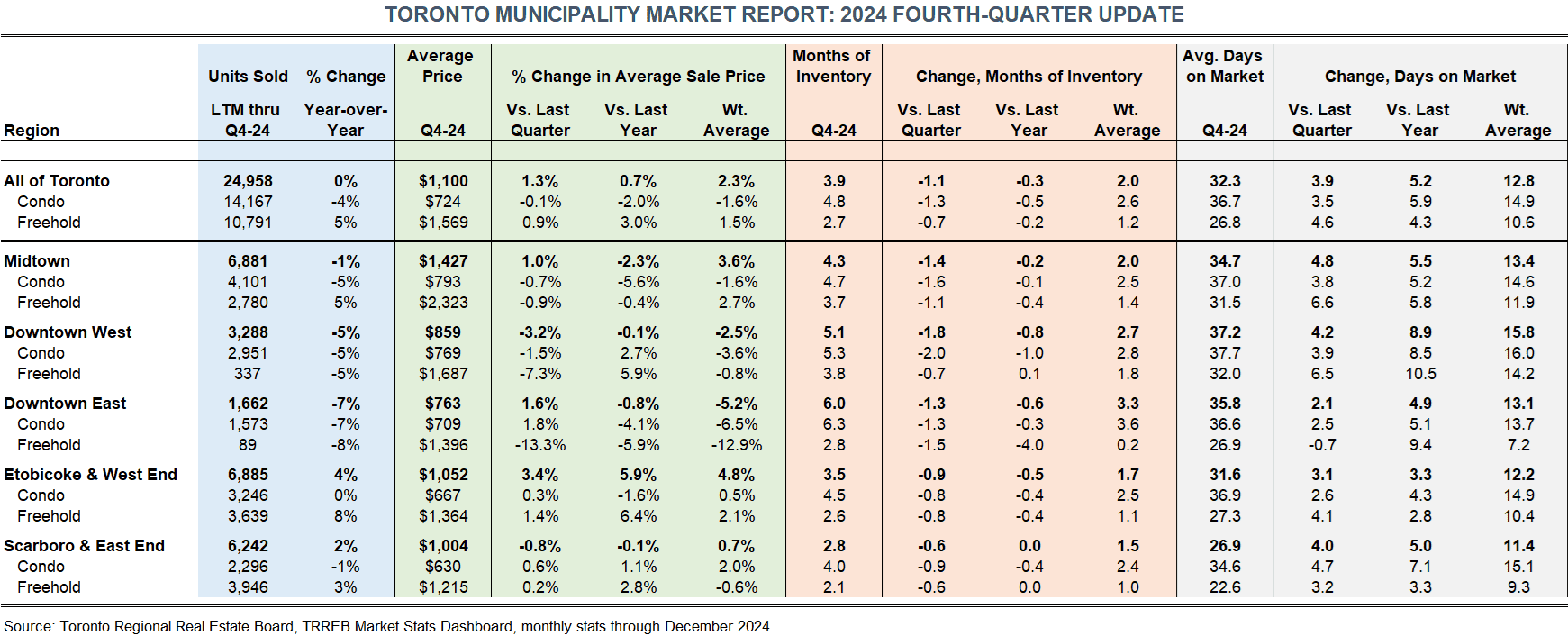

Average resale prices end 2024 largely unchanged from a year ago with freeholds outperforming condos; condo and freehold inventory declined in the fourth quarter across all Toronto boroughs but remain above the trailing 5-yr average

In 2022, the Greater Toronto Area, like other real estate markets across the country, saw a significant decline in sales activity. Resale units sold were down 38% year-over-year and 21% when compared to the trailing 5-year average. The slowdown in activity continued throughout 2023, with units sold down a further 12% year-over-year. At the end of 2024, resale activity came in lower than originally forecast, with only a 2.5% annual increase in sales from the depressed levels recorded in 2023. The Toronto Regional Real Estate Board (TRREB) compiles transaction data for each major market within the GTA, with historical sales data available for multiple decades. While historical trends should not be considered the sole indicator of what’s to come, they are helpful to review and consider as part of the broader context. In this year-end update, we'll outline transaction highlights for each of the communities comprising the municipality of Toronto, as well as overall performance by property type.

GTA Regional Overview

Toronto is the largest city in Canada and the economic and entertainment hub of our country. It is one of our most livable cities, although high home prices continue to put it at a disadvantage to other world-class Canadian cities such as Montreal and Calgary. Nevertheless, with strong immigration levels into our country and a growing population, Toronto will continue to be a major destination.

Beyond the Toronto municipality comprised of Toronto proper, Scarborough, and Etobicoke, TRREB covers the surrounding GTA regions of Orangeville, York, and Simcoe to the north, Halton and Peel to the west, and Durham to the east. In this report, we focus on the core Toronto municipality, which is the largest region for overall sales activity in the GTA, representing 33% of all resales in Q4-2024.

Toronto Municipality

Market Highlights

Across all communities included in the municipality of Toronto, the average sale price observed in the fourth quarter of 2024 was $1.1 million, up 1.3% from the prior quarter but more or less flat from a year ago. When filtered by property types, freehold average prices are up year-over-year while condos are down slightly and featuring close to double the inventory. Resale activity in Toronto proper remains sluggish, with condo sales down 4% from 2023 and freeholds only up 5%.

In the broader context, prices within Toronto proper have experienced less growth over the past 5 years than regions in the surrounding GTA like Pickering, Newmarket, and Brampton. This can be attributed to two things: (1) the relative affordability of these suburban markets surrounding Toronto, and (2) the pandemic’s impact on the need for more space at home. Compared to its average price 5 years ago, homes in Toronto proper are up 20%, while the entire GTA is up 30%. To compare Toronto’s performance against other major markets in the province, check out our article on Top Markets in Ontario here.

Going back more than 5 years, Toronto’s exceptional price growth have been driven by low supply of resale homes available for buyers. When your market has lots of demand, you need to have lots of people selling or lots of new homes being built. Toronto has neither of these when compared to the overall demand to live in or nearby the city. Add in the fact than many neighbourhoods in downtown Toronto have limited space for new development, such as Liberty Village, and it is evident that housing affordability will continue to be a big issue for the city. Over the trailing 5 years, Toronto has been a tight sellers’ market, with an average of two months of resale inventory.

Beginning in March 2022, multiple interest rate hikes resulted in a sharp cooling of the market, with Toronto ending the year with almost 3 months of resale inventory. After falling below 2 months during a strong spring market, back-to-back rate hikes in June and July resulted in inventory more than doubling to end 2023. In 2024, inventory declined for all property types and regions to start the year, rose across the board in the second and third quarters, and fell in the final quarter to sit just under 4 months of supply. Despite the fourth quarter decline, supply is still close to double the trailing 5-year average. Since 2020, Toronto properties have sold on average in 19 days. With more inventory and properties now selling in 32 days on average, market conditions are becoming more favourable for buyers, notwithstanding the higher costs of homes and associated mortgage interest.

Around 60% of properties in the Toronto municipality are condominiums, with the remainder being freehold properties such as detached and semi-detached houses. Housing mix varies widely depending on location, with over 90% of properties sold in the downtown core being condos. Toronto condos are about half the price of their freehold counterparts, with average sale prices in the fourth quarter of $724K and $1,569K respectively.

Through the fourth quarter, both property types continue to take longer to sell than a year ago, with condos taking 10 days longer to sell than freeholds. The condo segment has also seen greater supply available for buyers, close to double the trailing 5-year average at just under 5 months. Higher interest rates and monthly condo fees are pushing many buyers - and sellers with variable mortgages - out of this market. Freehold inventory decreased during the fourth quarter but remain constrained at just under 3 months of supply. With severely limited space available for the development of new freehold properties in the city, low inventory levels for freeholds will continue to be the norm. However, freehold supply is still slightly higher than its trailing 5 year average.

Community Overview

Downtown Toronto

Downtown Toronto is defined as the area south of Bloor, bounded by Etobicoke to the west and Scarborough to the east. The downtown core is further separated into its east and west districts by Yonge Street, the primary thoroughfare that runs north-south through the city.

Community Overview

Downtown West

Downtown West, defined by TRREB as the C01 community, is one of the most vibrant areas of the city. It features a variety of unique neighbourhoods such as Chinatown, Kensington Market, Trinity Bellwoods, Fort-York and its National Historic Site, King-West and the Fashion District, Little Italy, Liberty Village, and the Toronto harbourfront. Downtown West is also the hub of sports, entertainment, and tourism in the city. Popular tourist attractions include the CN Tower, the Ripley’s Aquarium, and Nathan Phillips Square at Toronto City Hall. Between Scotiabank Arena and the Rogers Centre, sporting events and concerts happen on almost a nightly basis, while other events such as Toronto FC soccer games and outdoor concerts take place at the CNE fairgrounds.

For those more interested in arts and culture, Downtown West is host to the Toronto International Film Festival every year, while the AGO and the ROM are two of the city’s most prominent museums. Alongside all these entertainment options, Downtown West features an array of world-class restaurants, bars, and retail, assuring that locals and tourists alike are never short on things to do.

Downtown West is close to fully developed, with over 90% of resale activity over the last twelve months pertaining to condominiums. In recent years, and accelerating now, the area has undergone significant housing intensification efforts through the development of various high-rise condos, such as those in the mixed-use “Well” development near Spadina and Front. This will add some additional supply to the market, but if demand grows as expected, low inventory should remain the norm.

Similar to the city as a whole, condos in Downtown West are about half the price of their freehold counterparts, down 4% year-over-year with an average sale price of $769K in Q4-2024. Despite a decline in supply to finish the year, condo inventory remains elevated with average selling times continuing to climb at 37 days. At 5.1 months of supply in Q4-2024, buyers have close to double the available units to choose from when compared to the trailing 5 years, limiting bidding wars and resulting in minimal price appreciation.

Community Overview

Downtown East

Downtown East, defined by TRREB as the C08 community, is one of the oldest and most historic parts of our country. In terms of land area and overall sales activity, it is about half the size of Downtown West, with a similar housing mix that is dominated by condos. Compared to Downtown West, condos in Downtown East are typically older, more spacious, and less associated with high-rise building formats.

Downtown East is home to many historic attractions, most notably the St. Lawrence Market and Distillery District. Both venues offer an array of food, shopping, and live entertainment, with much of the surrounding architecture dating back over a hundred years. During the holiday season, the Distillery District Winter Village is one of the city’s most popular events. St. Lawrence Market and the Distillery Districts are a short 15 minute walk from one another, making this historic area a must-see for tourists and locals alike. Closer to Bloor Street, the Toronto Metropolitan University is a major post-secondary institution, with a student population of close to 50K. The surrounding area caters to this younger demographic as well as the LGBTQ community, with a vibrant nightlife and restaurant scene centered around Church & Wellesley.

In the fourth quarter of 2024, Downtown East reported an average condo sale price of $709K, down 4% year-over-year. Like Downtown West, inventory ballooned following June and July rate hikes in 2023 and has remained relatively high at 6 months to end 2024. These supply levels are close to double what buyers have been used to since 2020. As expected from these high supply levels, properties in Downtown East are now taking 36 days to sell on average, 5 days longer than a year ago and continuing to lag all regions within Toronto proper.

Community Overview

Midtown Toronto

Midtown Toronto is the largest region in the Toronto municipality in terms of overall sales activity. It is also the most expensive, with an average price of $1,427K in the fourth quarter. Midtown Toronto is bounded by Bloor Street to the south, Steeles Avenue along the northern municipal boundary, and Etobicoke and Scarborough to the west and east. This area features a wide variety of neighbourhoods, such as Casa Loma and the Annex, Yonge & Eglington, Forest Hill, Don Mills, Bayview Village, and the infamous Bridlepath. Some of these neighbourhoods, such as the Bridlepath and Forest Hill, are comprised mostly of expensive freehold properties, while other neighbourhoods, such as Yonge & Eglington, are predominantly high-rise condos and older apartment complexes. Given the wide-variety within Midtown, it’s important to speak with a realtor knowledgable in your preferred location and property type in order to get a better sense of what – and where – you may be able to afford.

Collectively, resale activity in Midtown is about 60% condos, with a drastic difference in average price between the two property types. Condos in Midtown are similar to the downtown core, with an average sale price of $793K in the final quarter of 2024. Freeholds, on the other hand, are dramatically more expensive with an average price of $2.3 million in Q4-24. Compared to last year's fall market, Midtown prices are flat for freeholds and down 6% for condos. On an aggregated basis, Midtown continues to outperform the downtown core, up 4% compared to the trailing 5-year average resale price. Midtown's outperformance for price growth is driven by its greater share of detached homes, with this property type featuring limited new supply across all of Toronto proper.

During the fourth quarter, both property types in Midtown are taking longer to sell than they were a year ago, now at 35 days on average. At over 3 months of supply for both property types, inventory is in line with where it stood one year ago but significantly above the trailing 5-year average, driven by challenging market conditions for new buyers as well as mortgage-holders.

Community Overview

Etobicoke and the West End

Etobicoke and the West End, defined by TRREB as communities W01 thru W10, forms the entire western portion of the Toronto municipality, with similar resale activity to Midtown Toronto. Along Lake Ontario, the neighbourhoods of Roncesvalles, High Park, Mimico, and Long Branch are vibrant, densely populated, and growing fast, with condos and apartments making up a greater share of the current housing mix. Being relatively close to Downtown West and surrounded by parks and waterfront, this sub-region within Etobicoke will continue to see new development and housing intensification efforts.

North of the Gardiner highway, Etobicoke neighbourhoods such as Sunnylea and Princess Rosethorn have a greater share of freehold properties, featuring more spacious lots and suburban qualities than what is found in Toronto or even South Etobicoke. With the Humber River weaving its way through the city, Etobicoke features a multitude of trails, parks, and golf courses, while also offering shopping, entertainment, and quick access to Toronto. For these reasons, it has historically been a popular place for those in downtown Toronto to “give up the city dream” and upgrade to a family home complete with two-car garage. Collectively, Etobicoke's current housing mix is split equally between freeholds and condos, although condos continue to grow in prominence.

During the fourth quarter, the average sale price in Etobicoke was around $1,052K, up 6% year-over-year. However, when normalizing for shifting housing mix across different periods, freeholds have driven price growth while condos in Etobicoke are down 2% from a year ago. Freeholds in Etobicoke ended the year at $1,364K, roughly twice the price of an Etobicoke condo at $667K in Q4-2024. Etobicoke inventory fell to start 2024, rose for both property types in the second and third quarters before declining to end the year. Compared to the trailing 5-year average, buyers have close to double the supply to choose from, although freehold inventory remains relatively tight at 2.6 months. Like all regions in Toronto, properties in Etobicoke are also taking longer to sell than a year ago, now 32 days on average with condos taking 10 days longer to sell than Etobicoke freeholds.

Community Overview

Scarborough and the East End

Scarborough and the East End, defined by TRREB as communities E01 through E11, forms the entire eastern portion of the Toronto municipality, with overall resale activity slightly less than Midtown Toronto and Etobicoke. Starting along the lakeshore, the region is bounded to the west by the Don Valley Parkway, while Victoria Park Avenue forms the remainder of its western boundary up to Steeles Avenue. Close to Downtown East, the neighbourhoods of Danforth, Leslieville, and the Beaches feature some of the best restaurants and music venues in the city. With close proximity to downtown Toronto, these neighbourhoods offer the appeal of the city without the high-rise condo and office towers.

East of Victoria Park Avenue and towards the Pickering townline, Scarborough features a greater share of suburban neighbourhoods comprised of detached and semi-detached homes. The area also has an abundance of green space, both along the lakeshore escarpment and throughout the city interior. Notable attractions include the Scarborough Bluffs, one of the most popular lookouts in the GTA, the Toronto Zoo, the largest in the country, and Rouge National Urban Park. Prominent neighbourhoods within East Scarborough include Cliffcrest, Woburn, and Agincourt. Collectively, Scarborough features the greatest share of freehold properties in the city, with only 37% of homes sold relating to condominiums.

Historically and to this day, Scarborough & East End is the most affordable region within Toronto, with average prices of $630K for condos and $1,215K for freeholds in the fourth quarter. Across all properties, the Scarborough average price is more or less unchanged from a year ago, with condos outperforming freeholds over the past 5 years.

Notably, freehold properties in Scarborough continue to have the lowest inventory in the city. Across all Scarborough homes, resale inventory averaged 2.8 months in the fourth quarter. As expected from this limited supply, properties in Scarborough continue to sell faster than anywhere in the city, with Scarborough freeholds selling relatively quickly at 27 days on average. However, with many buyers continuing to hold out for lower rates, selling times are higher than a year ago.

Community Overview

Surrounding GTA

After outperforming in 2022, price growth in Toronto proper is back in line with the surrounding GTA, both up 2% in 2023 and flat to end 2024. The surrounding GTA experienced a more significant correction during 2022 and is well below its pandemic peak for average sale prices. North of the Toronto municipal boundary at Steeles Avenue, York region consists of a variety of high-growth, expensive cities such as Markham, Richmond, Newmarket, and Aurora. Further north are the regions of Simcoe and Dufferin, which include the cities of Orangeville, Innisfil, and Bradford. In the fourth quarter of 2024, York region had an average sale price of $1,297K, up 1% year-over-year, while Simcoe and Dufferin are more affordable at $823K (up 4.2% YoY) and $981K (up 3.8% YoY) respectively.

To the west of Etobicoke, regions covered by TRREB include Peel and Halton. Peel region includes the cities of Brampton and Mississauga, while Halton includes luxury Oakville, Milton, and Burlington markets. During the fourth quarter, Peel region recorded an average sale price of $1,037K, down 0.8% from a year ago, while Halton’s average sale price of $1,227K was down 1.3% year-over-year. Finally, east of the Pickering-Scarborough townline, TRREB covers the Durham region, which includes the cities of Ajax, Pickering, Whitby, and Oshawa, amongst others. Durham region had an average sale price of $902K in the fourth quarter, up 0.4% year-over-year.

Archived Reports

Toronto & GTA

Third Quarter 2023 Market Report

Second Quarter 2023 Market Report

Summary

The Toronto Market report will be updated on a quarterly basis. Every market is different, but understanding available inventory levels alongside recent price and market trends can help prospective buyers and sellers make more informed decisions. Subscribe to quarterly updates of the Toronto Market Report by completing the contact form below.

Thank you for taking the time to read this article. As you contemplate the next steps in your real estate journey, there are a variety of helpful online resources you can leverage, such as realtor.ca, the Canadian Mortgage and Housing Corp, and historical sales data and market insights from leading real estate websites like Zolo, Royal LePage, HouseSigma, and Wahi.