Toronto Market Report

2023 Third Quarter Update

An overview of historical transaction data in the municipality of Toronto

In 2022, the Greater Toronto Area, like other real estate markets across the country, saw a significant decline in sales activity. Resale units sold were down 38% year-over-year and 21% when compared to the trailing 5-year average. After a strong pickup in sales activity and average prices during the second quarter of 2023, consecutive rate hikes in June and July dampened buyer demand, with inventory rising sharply and average prices down 8%. The Toronto Regional Real Estate Board (TRREB) compiles transaction data for each major market within the GTA, with the TRREB Market Stats dashboard providing historic sales data going back to 1996. While historical stats should never be the sole indicator of what’s to come, they are helpful to review and consider as part of the broader context. In this article, we'll outline latest transaction highlights for each of the communities comprising the municipality of Toronto, as well as overall performance by property type.

GTA Regional Overview

Toronto is the largest city in Canada and the economic and entertainment hub of our country. It is one of our most livable cities, although high home prices continue to put it at a disadvantage to other world-class Canadian cities such as Montreal and Calgary. Nevertheless, with strong immigration levels into our country and a growing population, Toronto will continue to be a major destination.

Beyond the Toronto municipality, which is comprised of Toronto, Scarborough, and Etobicoke, TRREB covers the surrounding GTA regions of Orangeville, York, and Simcoe to the north, Halton and Peel to the west, and Durham to the east. In this report, we will focus on the core Toronto municipality, which is the largest region for overall sales activity in the GTA, representing 37% of all resales over the last twelve months.

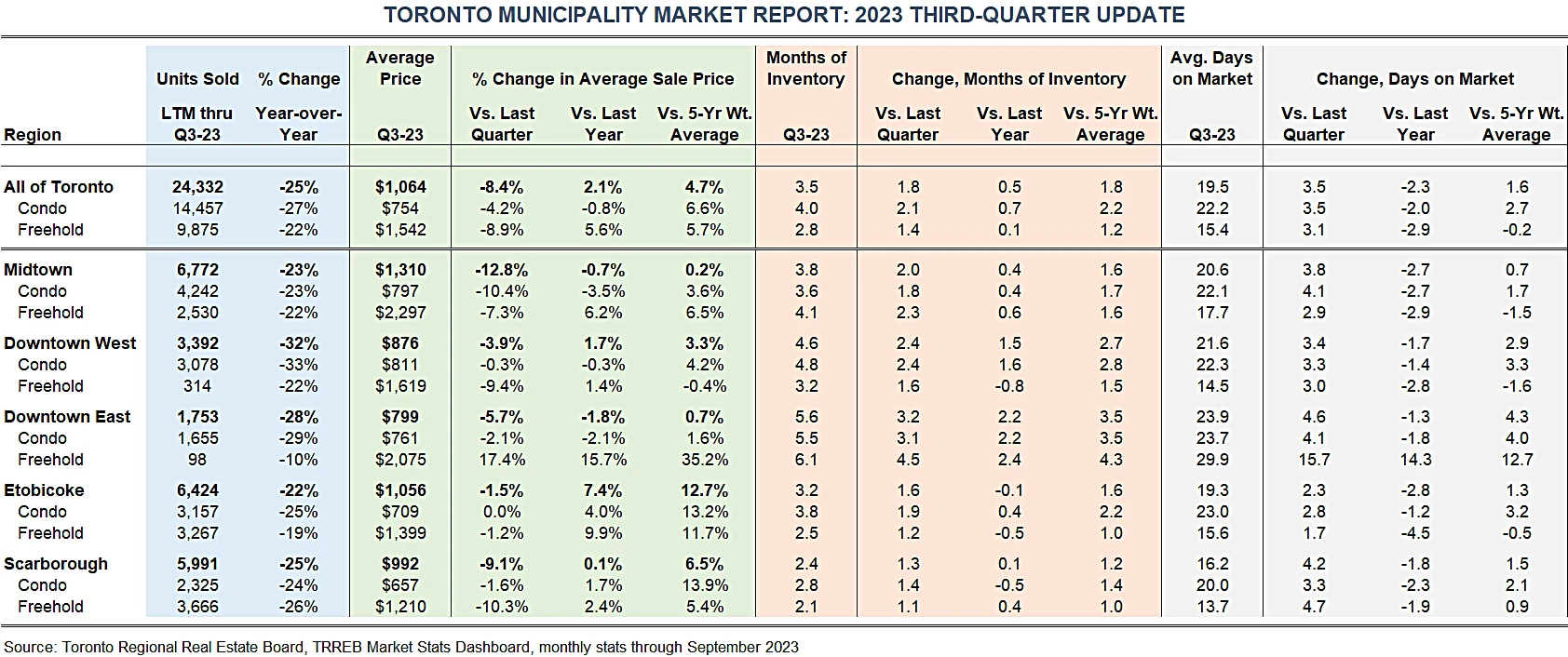

Toronto Municipality

Total Market Overview

Across all communities included in the municipality of Toronto, the average sale price observed in the third quarter of 2023 was $1.06 million, up 2.1% year-over-year but down 8.4% from the second quarter. During 2022 and through the first quarter of 2023, demand was more resilient in the core Toronto municipality, while in recent quarters the surrounding GTA has performed better, with prices up 2.7% year-over-year.

Despite Toronto’s relative outperformance in 2022 compared to the surrounding GTA (and province) as a whole, in the broader context, prices within Toronto proper have experienced less growth over the past 5 years than regions in the surrounding GTA like Pickering, Newmarket, and Brampton. This can be attributed to two things: (1) the relative affordability of these suburban markets surrounding Toronto, and (2) the pandemic’s impact on the need for more space at home. To compare Toronto’s performance against other major markets in the province, check out our article on Top Markets in Ontario here.

Going back further than 5 years, Toronto’s exceptional price growth has been driven by its low inventory, or housing supply available for buyers. When your market has lots of demand, you need to have lots of people selling or lots of new homes being built. Toronto has neither of these when compared to the overall demand to live in or nearby this city. Add in the fact than many neighbourhoods in downtown Toronto have limited space for new development, such as Liberty Village, and it is evident that housing affordability will continue to be a big issue for the city. Over the trailing 5 years, Toronto has been a tight sellers’ market, with an average of just under two months of resale inventory.

Throughout 2022, multiple interest rate hikes resulted in a temporary cooling of the market, with Toronto ending the year with almost 3 months of available inventory, up slightly from where it’s been since 2017. During the first half of 2023, inventory and selling times both fell steadily, indicating that some buyer demand was coming back to market. However, after consecutive 25 basis-point rate hikes in June and July, inventory levels doubled during the third quarter, now back above 3 months with homes also taking 4 days longer to sell. With prices stable but interest rates holding at the highest level in 22 years, many buyers remain on the sidelines.

Around 60% of properties in the Toronto municipality are condominiums, with the remainder being freehold properties such as detached and semi-detached houses. Housing mix varies widely depending on location, with over 90% of properties sold in the downtown core being condos. Toronto condos are about half the price of their freehold counterparts, with average sale prices in the third quarter of $754K and $1,542K respectively, both down from the second quarter where prices peaked in May. Despite the relative affordability, Toronto condos are not performing as well as freeholds, down 0.8% year-over-year. With limited new freehold supply coming to Toronto proper, it is likely that this property segment will continue to see prices grow at a faster rate than condos.

During the third quarter, both property types are taking longer to sell, with condos taking a week longer to sell than freeholds on average. The condo segment continues to see greater inventory levels available for buyers, with supply doubling for both property types in the third quarter. Freehold inventory now sits at 2.8 months while condos are up to 4 months. With severely limited space available for the development of new freehold properties in the city, lower inventory levels for freeholds will continue to be the norm.

Community Overview

Downtown Toronto

Downtown Toronto is defined as the area south of BloorStreet, bounded by Etobicoke to the west and Scarborough to the east. The downtown core is further separated into its east and west districts by Yonge Street, the primary thoroughfare that runs north-south through the city.

Community Overview

Downtown West

Downtown West, defined by TRREB as the C01 community, is one of the most vibrant areas of the city. Downtown West is close to fully developed, with over 91% of resale activity over the last twelve months pertaining to condominiums. In recent years, and accelerating now, the area has undergone significant housing intensification efforts through the development of various high-rise condos, such as those in the mixed-use “Well” development near Spadina and Front. This will add some additional supply to the market, but if demand grows as expected, low inventory levels will persist throughout the downtown core.

Similar to the city as a whole, condos in Downtown West are about half the price of their freehold counterparts, steady in the third quarter with an average sale price of just over $800K. Compared to a year ago, condos in Downtown West are flat while freeholds are up slightly (1.4%). Both property types saw inventory fall in the second quarter before doubling between July and September.

Community Overview

Downtown East

Downtown East, defined by TRREB as the C08 community, is one of the oldest and most historic parts of our country. In terms of land area and overall sales activity, it is about half the size of Downtown West, with a similar housing mix that is dominated by condos. Compared to Downtown West, condos in Downtown East are typically older, more spacious, and less associated with high-rise building formats.

In the third quarter of 2023, Downtown East reported an average sale price of $799K, erasing strong gains recorded in the second quarter and down 2% year-over-year. After inventory steadily grew in 2022 to finish the year at double the preceding 5-year average for supply, the first half of 2023 saw a decline in inventory for both property types to move back in line with the trailing 5-year average. However, supply rose sharply in the third quarter, with both property types reporting the highest inventory levels in Toronto at 5.5 months for condos and 6.1 months for freeholds.

Community Overview

Midtown Toronto

Midtown Toronto is the largest region in the Toronto municipality in terms of overall sales activity. It is also the most expensive, with an average price to end the third quarter of $1,310K. Collectively, resale activity in Midtown is about 60% condos, with a drastic difference in average price between the two property types. Condos in Midtown are similar to the downtown core, falling 10% during the third quarter with an average price of $797K. Freeholds, on the other hand, are dramatically more expensive at an average price of $2.3 million. Year-over-year, condo prices in Midtown are down 3.5%, underperforming Midtown freeholds (+6.2%), the Toronto municipality (+2.1%), and the GTA as a whole (+2.5%).

During the third quarter, Midtown condos took 5 days longer to sell than freeholds, with both property types reporting a sharp reversal in supply. Resale inventory in Midtown is now back to double its trailing 5-year average, more or less in line with supply levels recorded during the third quarter of 2022.

Community Overview

Etobicoke and the West End

Etobicoke and the West End, defined by TRREB as communities W01 thru W10, forms the entire western portion of the Toronto municipality, with overall resale activity more or less in line with Midtown Toronto. Collectively, the Etobicoke housing mix is split equally between freeholds and condos, although condos will continue to grow in prominence.

During the third quarter, the average sale price in Etobicoke was just under $1.06 million, up 7% year-over-year to be the best performing region in the Toronto municipality. Condos in Etobicoke are performing more or less in line with the freehold segment over the past 5 years , where they are up 13%. Freeholds in Etobicoke sold on average for $1,400K during the third quarter, roughly twice the price of an Etobicoke condo.

Etobicoke inventory of both condos and freeholds had fallen for each of the last three quarters, finishing the first half of the year at under 2 months. Like other GTA markets, supply rose sharply in the latest quarter, with both property types now reporting more supply than their trailing 5-year averages.

Community Overview

Scarborough and the East End

Scarborough and the East End, defined by TRREB as communities E01 through E11, forms the entire eastern portion of the Toronto municipality, with overall resale activity slightly less than Midtown Toronto and Etobicoke. Starting along the lakeshore, the region is bounded to the west by the Don Valley Parkway, while Victoria Park Avenue forms the remainder of its western boundary up to Steeles Avenue.

East of Victoria Park Avenue and towards the Pickering townline, Scarborough features a greater share of suburban neighbourhoods comprised of detached and semi-detached homes. Prominent neighbourhoods within East Scarborough include Cliffcrest, Woburn, and Agincourt. Collectively, Scarborough features the greatest share of freehold properties in the city, with only 39% of resales over the past twelve months relating to condominiums.

Historically, and to this day, Scarborough is the most affordable region within Toronto, ending the third quarter with average prices of $657K for condos and $1,210K for freeholds. Across all properties, the Scarborough average price is flat on a year-over-year basis. When compared to other regions in Toronto proper, Scarborough trails only Etobicoke for price growth when compared to its trailing 5-year average. The relative affordability offered by Scarborough results in it having the lowest supply of homes of all regions in Toronto, something that has been the norm for most of the past 5 years.

Like other neighbourhoods in the municipality, Scarborough inventory for both freeholds and condos roughly doubled in the third quarter, now sitting at just two and half months of supply. Properties in Scarborough continue to sell faster than anywhere in the city, although both freeholds and condos are taking longer to sell when compared to the previous quarter.

Community Overview

Surrounding GTA

North of the Toronto municipal boundary at Steeles Avenue, York region consists of a variety of high-growth, expensive cities such as Markham, Richmond, Newmarket, and Aurora. Further north are the regions of Dufferin and Simcoe, which include the cities of Orangeville, Innisfil, and Bradford. During the third quarter, York region had an average sale price of $1,343K, up 6.6% year-over-year, while Simcoe and Dufferin are more or less flat.

To the west of Etobicoke, regions covered by TRREB include Peel and Halton. Peel region includes the cities of Brampton and Mississauga, while Halton includes the cities of Oakville, Milton, and Burlington. During the third quarter, Peel region recorded an average sale price of $1,060K, up 0.4% from a year ago, while Halton’s average sale price of $1,246K is up 1.4%. Finally, east of the Pickering-Scarborough townline, TRREB covers the Durham region, which includes the cities of Ajax, Pickering, Whitby, and Oshawa, amongst others. Durham region ended the year with an average sale price of $935K, up 2.5% year-over-year.

Despite year-over-year price gains, average prices across all surrounding GTA regions fell from the second quarter, with higher rates worsening affordability challenges.

Archived Reports

Toronto & Area Market Updates

Second-Quarter 2023 Market Report

Summary

The Toronto Market report will be updated on a quarterly basis. Every market is different, but understanding available inventory levels alongside recent price and market trends can help prospective buyers and sellers make more informed decisions. A summary of all Toronto markets through the third quarter of 2023 is presented above and you can subscribe to quarterly updates of the Toronto Market Report by completing the contact form below.

Thank you for taking the time to read this article. As you contemplate the next steps in your real estate journey, there are a variety of helpful online resources you can leverage, such as realtor.ca, the Canadian Mortgage and Housing Corporation, and historical sales data and market insights from leading real estate websites like Zolo, Royal LePage, HouseSigma, and Wahi.