London Market Report

2024 Second Quarter Update

London prices increasing but remain down 2% year-over-year; inventory notably increased in the second quarter and now sits close to double the trailing 5-year average

Over the last two years, the Greater London Area, like other real estate markets across the country, saw a significant decline in sales activity. Resale units sold in 2022 was down 29% when compared to the record year in 2021 before falling another 13% in 2023. Muted market activity has continued through the first half of 2024, with overall sales down 3% year-over-year. The Canadian Real Estate Association (CREA), through its various real estate boards and provincial associations, compiles transaction data for each of its major markets, with the CREA Stats Centre reporting sales data going as far back as 1980. While historical stats should never be the sole indicator of what’s to come, they are helpful to review and consider as part of the broader context. In this article, we'll outline second-quarter transaction highlights for each of the communities comprising the London Area as well as overall performance by property type.

Greater London Area: Regional Overview

London, the seat of Middlesex County, is the largest city in southwestern Ontario and the 11th largest metropolitan area in Canada. With close proximity to the GTA, Michigan and New York state borders, and multiple Great Lakes, the region is well-poised for future growth. It is the economic hub of southwestern Ontario, with major companies, hospitals, and higher education based in the city. For anyone familiar with London, the signs of new housing development are everywhere, with significant urban sprawl occurring throughout north and west London.

30 minutes south of London is St. Thomas, the seat of Elgin County. Ten minutes beyond St. Thomas, Port Stanley and other beach towns along Lake Erie offer recreational getaways for London locals. A similar drive west of the city are the towns of Komoka-Kilworth and Strathroy-Caradoc, with a short drive further to reach the shores of Lake Huron. East of London, in Oxford County, are the growing towns of Woodstock, Ingersoll, Tillsonburg, and Norwich. With both the 401 and 402 highways running along the southern border of London, surrounding Middlesex County and these neighbouring communities are easily accessible. For this reason, they can be considered part of the Greater London Area.

Greater London Area: Total Market Overview

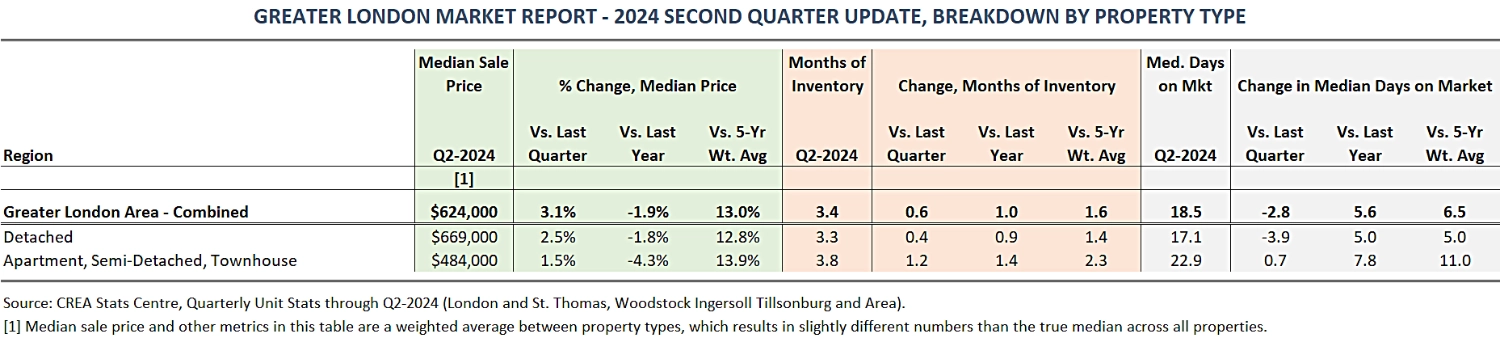

Across all communities included in the GLA, the second-quarter median sale price was around $624K, up slightly from the prior quarter but down 1.7% year-over-year.

Despite minimal price growth over the past two years, London prices have experienced significant growth since 2018, outperforming neighbouring markets like Kitchener-Waterloo, Hamilton, and the GTA. This can be widely attributed to the relative affordability of London homes when compared to similar ones in these nearby markets. For the preceding 20 years, London prices have more or less lagged behind the growth experienced in these markets, and it appears that recently the Forest City has been playing catch-up. Compared to the average price recorded in Q1-2019, London homes are now up 60%, which represents an annual growth rate of 9.8%. To compare London’s performance against other major markets in the province, check out our article on Top Markets in Ontario here.

Part of what drove London’s staggering price growth during the pandemic was its shortage of housing supply available for buyers. To end the 2021 year, the Greater London Area had only 0.4 months of inventory, meaning that listed homes were selling in under two weeks on average. Without new homes hitting the market, London inventory would have disappeared in less than a month. When inventory levels are this low, prices have to rise on account of too many buyers bidding on too few properties. This leads to bidding wars and runaway prices which were consistent themes during the market peak in early 2022. Over the trailing 5 years, the GLA has been a tight sellers’ market, with less than 2 months of resale inventory.

Beginning in March 2022 and extending into 2023, multiple interest rate hikes resulted in a market slowdown, with London ending the year with 4.4 months of available inventory, more than double the historical supply recorded since 2018. After inventory fell during the first quarter, supply notably increased back above 3 months during a slower than expected spring market. Homes are taking longer to sell at 18 days, up from a median 13 days during 2023 spring market. In London and across the province, buyers have not re-entered the market as expected.

Most properties in the Greater London Area, about 3 out of 4, are detached homes. Detached homes in London, as expected, are more expensive than apartments and semi-detached properties, with median sale prices to end the year of $669K and $484K respectively. Over the past 5 years, detached homes in Greater London have seen prices grow at a slightly slower pace than the apartment segment, which has nearly doubled in value since the first quarter of 2019. During the second quarter, detached homes are selling 6 days faster than the apartment segment, with both property types taking longer than a year ago and trailing 5-year average.

Community Overview

London North, London South, and London East

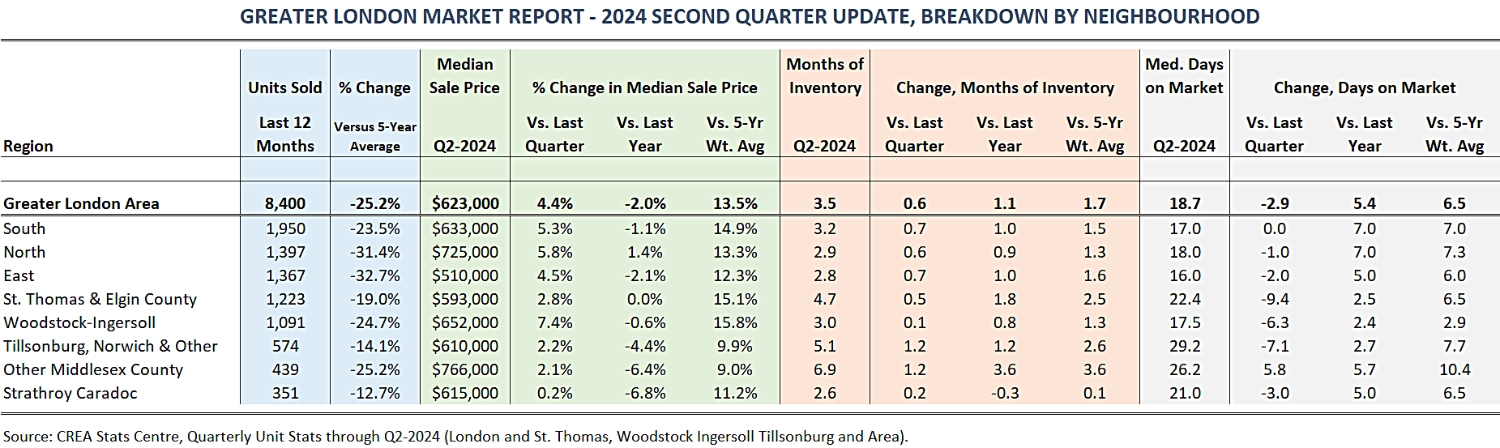

These three boroughs each have multiple neighbourhoods within them, and in total account for close to 60% of resale activity in Greater London. During the second quarter, London proper is featuring more balanced conditions than a year ago, with both inventory and selling times up year-over-year across all three boroughs.

Despite similar trends for inventory and median days on market, London proper features drastically different house prices across the city. London North leads the way, with a median sale price in the second quarter of $725K, up 1.4% year-over-year. This area is characterized by high-growth, newer developments such as those in Masonville and Sunningdale as well as the big-box retail and new homes surrounding Fanshawe & Hyde Park. London East, historically and to this day, is the most affordable of the three boroughs, with a Q2-2024 median sale price of $510K. This area has the most diverse housing mix in the city, which includes historic luxury properties along the Thames River downtown, an array of apartments and multi-units in the downtown core, and smaller, more affordable detached homes east of Adelaide Street. Given this wide-variety, it’s important to speak with a realtor knowledgeable in your preferred location and property type in order to get a better sense of what – and where – you may be able to afford. Despite inventory growing in the second quarter, London East continues to feature the lowest supply of resale homes across London proper. Finally, London South ended the year with a median sale price of $633K, down slightly year-over-year but up from the first quarter. Prominent neighbourhoods in South London include Wortley Village, Byron and Springbank Park, and White Oaks.

Community Overview

St. Thomas and Elgin County

In terms of overall resale units sold, St. Thomas & Elgin County is fourth largest GLA region after London South, North, and East. While sales activity is still down from historical levels, it remains a more active market than London, with unit sales over the past 12 months only down 19% when compared to the trailing 5-year average.

During the second quarter, St. Thomas and Elgin County reported a median sale price of $593K, gaining on the prior quarter and flat year-over-year. After inventory steadily grew in 2023 to end the year with over 5 months, resale supply tightened to start the new year but increased in the second quarter. When compared to the trailing 5-year average, buyers still have close to twice the homes to choose from.

As expected from increased relative supply, homes in St. Thomas and Elgin County are taking a long time to sell, with a median listing period of 22 days, up 2 days from median selling times observed one year ago.

Community Overview

Woodstock-Ingersoll

The next largest region within Greater London is Woodstock-Ingersoll, more or less similar in population and unit sales to St. Thomas and Elgin County. It is a unique smaller market, with direct access via the 401 to larger cities such as London to the west and the tri-cities and Brantford to the east.

Woodstock-Ingersoll recorded a median sale price of $652K in the second quarter, up 7% from the prior quarter but flat on a year-over-year basis. When compared to its trailing 5-year average, the median price is up 16%, outperforming all other regions in the Greater London Area.

At the start of 2022, inventory levels in Woodstock were critically low, with only about two weeks of inventory. This supply-demand imbalance is why prices in Woodstock-Ingersoll were up 30% in 2021. In 2023, Woodstock-Ingersoll saw inventory levels grow in the third and fourth quarters, ending the year with close to 5 months of available supply. Inventory fell 2 months to start the year and stayed around 3 months during the second quarter. Compared to the 2023 spring market, there is more resale inventory which is reflected in median selling times which is up slightly at 17-18 days.

Community Overview

Tillsonburg & Area

Tillsonburg & Area has experienced strong growth in recent years, with the 2021 census recording population growth of 18% since 2016, significantly outpacing the overall province (5%) and London (10%).

Tillsonburg & Area started the year with a median sale price of $594K, up slightly in the second quarter at $610K. In 2022, inventory increased more than ten-fold, ending the year at 8 months, the highest level for all regions within Greater London. As expected in conjunction with this increased supply, homes were also taking much longer to sell, leading all GLA regions at 38 days. Through the second quarter of 2024, inventory sits at 5 months of supply, more than double the trailing 5-year average with homes still taking longer than anywhere in Greater London to sell at 29 median days.

A final note regarding Tillsonburg & Area is that prices are drastically more expensive in the surrounding rural communities when compared to the town of Tillsonburg, which can result in large swings in prices based on what type of properties sell during a specific time period. As always, speak with a realtor experienced in your preferred location to get more refined estimates on how a specific neighbourhood may be shifting.

Community Overview

Surrounding Middlesex County

Surrounding Middlesex County, while only 5% of current resale activity, remains the most expensive market in Greater London, ending the second quarter with a median sale price of $766K. New housing development is rapidly progressing in many townships within this region, with most projects focused on single-family detached subdivisions with premium price points. Median prices are up from the previous quarter but down 6% year-over-year, driven from the highest inventory levels across the London area. At year-end 2022, inventory stood at 6 months, declined to 3 months by the second quarter of 2023 before drastically increasing to finish the year at over 10 months of inventory. Through the first half of 2024, inventory sits at 7 months with median selling times up 6 days.

Community Overview

Strathroy-Caradoc

Strathroy recorded a median sale price of $615K in the second quarter, flat from the prior quarter but down 7% year-over-year. When compared to the trailing 5-year average, Strathroy is up 11% which puts it slightly behind London proper. Strathroy has experienced drastic fluctuations in resale supply, ending 2022 with 5 months of inventory, falling to 2.7 months through the second quarter of 2023 before ending 2023 with over 6 months. Inventory fell the most of all London regions to start 2024, with supply declining by 4 months to sit at 2.5 months of supply in the first quarter and holding steady since. Compared to a year ago, homes are taking 5 days longer to sell.

Archived Reports

London & Area Market Updates

Third Quarter 2023 Market Report

Second Quarter 2023 Market Report

Summary

The Greater London Market report will be updated on a quarterly basis. Every market is different, but understanding available inventory levels alongside recent price and market trends can help prospective buyers and sellers make more informed decisions. You can subscribe to quarterly updates of the London Market Report report by completing the contact form below.

Thank you for taking the time to read this article. As you contemplate the next steps in your real estate journey, there are a variety of helpful online resources you can leverage, such as realtor.ca, the Canadian Mortgage and Housing Corp, and historical sales data and market insights from leading real estate websites like Zolo, Royal LePage, HouseSigma, and Wahi.